D.C. Circuit Review – Reviewed: Covid, Concealed Carry, and Unconstitutional Offsets

I’m traveling this weekend. So I decided to cheat with my post. Instead of taking time to explain the D.C. Circuit’s opinions this week, I asked ChatGPT to summarize them for me.

First, I asked ChatGPT to “Summarize Warren Harris v. Muriel Bowser from DC Circuit.” This is what I learned:

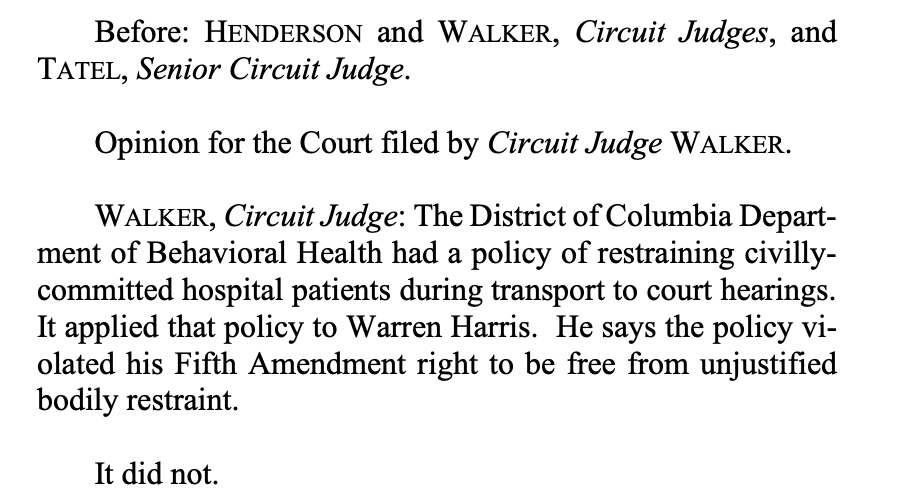

In Warren Harris v. Muriel Bowser, the DC Circuit Court considered a lawsuit filed by a group of churches challenging the District of Columbia’s COVID-19 restrictions on religious gatherings. The churches argued that the restrictions violated their First Amendment rights to free exercise of religion.

The court ruled in favor of the District of Columbia, upholding its COVID-19 restrictions as constitutional. The court found that the District’s restrictions were neutral and generally applicable, meaning that they applied to both religious and secular gatherings in the same way. The court also found that the District had a compelling interest in protecting public health during the pandemic, and that its restrictions were narrowly tailored to further that interest.

The court rejected the churches’ argument that the District’s restrictions were discriminatory or targeted at religious gatherings, noting that the District had applied the same restrictions to secular gatherings such as concerts and sporting events. The court also rejected the churches’ argument that they were being treated unfairly compared to other businesses or activities, such as grocery stores or protests, finding that these activities were not comparable to religious gatherings in terms of the risk of COVID-19 transmission.

Overall, the DC Circuit Court upheld the District of Columbia’s COVID-19 restrictions as constitutional and valid exercises of its police power to protect public health.

Hmm. Maybe I should be more precise. So I tweaked my request: “Summarize Warren Harris v. Muriel Bowser, No. 21-7122, from DC Circuit.” The response?

Warren Harris v. Muriel Bowser was a case heard by the DC Circuit Court, in which a plaintiff challenged a District of Columbia law that prohibited the carrying of concealed firearms in public places without a license.

The court upheld the constitutionality of the District of Columbia’s concealed carry law, finding that it did not violate the Second Amendment or the Due Process Clause of the Fourteenth Amendment. The court reasoned that the Second Amendment protects the right to keep and bear arms for self-defense, but that this right is not unlimited and may be subject to reasonable regulation.

The court found that the District of Columbia’s concealed carry law was a reasonable regulation designed to promote public safety and prevent gun violence. The court noted that the law did not ban the possession of firearms or prevent individuals from carrying firearms in non-public places, but rather only required individuals to obtain a license before carrying a concealed firearm in public.

The court also rejected the plaintiff’s argument that the District of Columbia’s concealed carry licensing scheme violated his Due Process rights by requiring him to demonstrate a good reason for carrying a concealed firearm. The court found that the licensing scheme provided sufficient procedural safeguards, including notice and an opportunity to be heard, and that the requirement to demonstrate a good reason was not an unconstitutional burden on the right to bear arms.

Overall, the court concluded that the District of Columbia’s concealed carry law was a constitutionally permissible regulation of the Second Amendment right to bear arms, and it upheld the law’s constitutionality.

Okay, but what about the Court’s other opinion? “Summarize Bradley Waterman v. IRS from DC Circuit.”

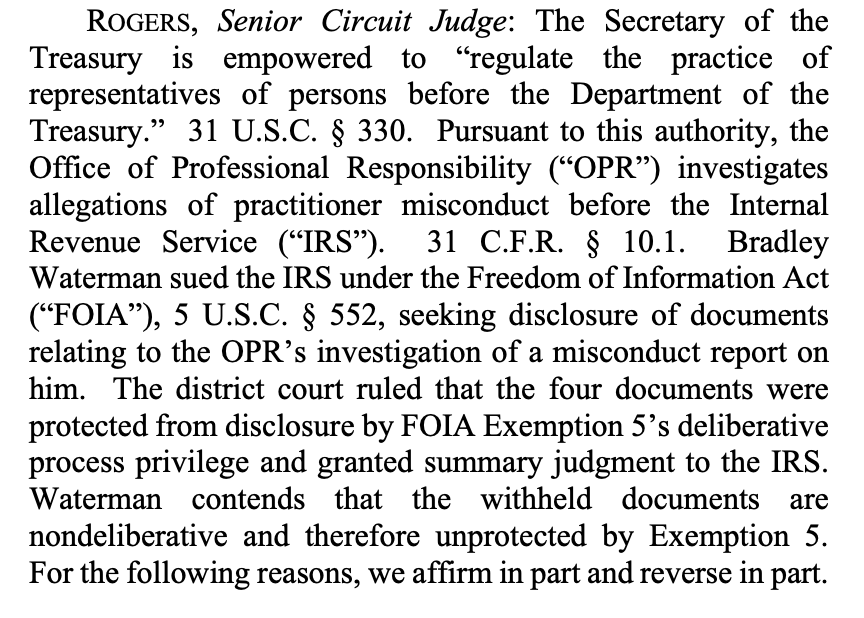

Bradley Waterman v. IRS was a case before the DC Circuit Court involving a dispute over tax liability. The plaintiff, Bradley Waterman, argued that he did not owe taxes on a distribution from his IRA because he had already paid taxes on the money when he contributed it to the IRA.

The court ruled against Waterman, finding that he was still liable for taxes on the distribution. The court explained that although taxpayers are generally not required to pay taxes on contributions to an IRA, they are required to pay taxes on distributions from the IRA. The court also rejected Waterman’s argument that he should be exempt from taxes on the distribution because he had already paid taxes on the underlying income, noting that the tax code requires taxpayers to pay taxes on distributions from their IRAs regardless of whether they have already paid taxes on the underlying income.

Overall, the DC Circuit Court upheld the IRS’s assessment of tax liability against Waterman, finding that he was required to pay taxes on the distribution from his IRA.

Wait a second. There is a dissent in Waterman: “Summarize Judge Justin Walker’s dissent in Bradley Waterman v. IRS from DC Circuit.”

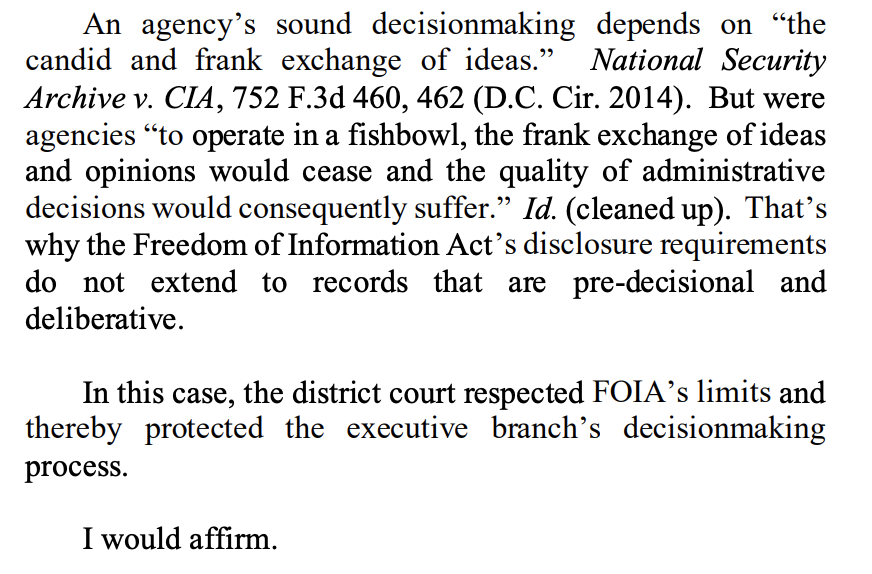

In Bradley Waterman v. IRS, Judge Justin Walker wrote a dissenting opinion arguing that the IRS’s offset of the taxpayer’s tax refund violated his constitutional rights.

Judge Walker argued that the taxpayer’s right to due process was violated because the IRS’s notices did not provide him with enough information about the basis for his tax debt or the procedures for contesting it. Judge Walker criticized the IRS’s use of a “one-size-fits-all” notice that did not provide any explanation or justification for the tax debt, which he believed left the taxpayer without meaningful notice or an opportunity to be heard.

Judge Walker also argued that the taxpayer’s right to equal protection was violated because the IRS’s offset procedures treated taxpayers with prior-year tax debts differently from taxpayers without such debts. Judge Walker believed that the offset procedures should have been subject to strict scrutiny, the highest level of judicial review, because they affected a fundamental right (the right to property) and discriminated against a suspect class (taxpayers with prior-year tax debts). Judge Walker argued that the government had not met its burden of showing that the offset procedures were narrowly tailored to serve a compelling government interest.

Overall, Judge Walker’s dissenting opinion in Bradley Waterman v. IRS argued that the taxpayer’s due process and equal protection rights were violated by the IRS’s offset of his tax refund, and he would have reversed the district court’s decision and remanded the case for further proceedings.

Once again, maybe I need to be more precise: “Summarize Bradley Waterman v. IRS, No. 21-5258, from DC Circuit.”

Bradley Waterman v. IRS was a case heard by the DC Circuit Court, in which a taxpayer challenged the IRS’s decision to reduce his tax refund to offset a prior-year tax debt. The taxpayer argued that this offset violated his constitutional rights to due process and equal protection.

The court ruled in favor of the IRS, upholding its authority to offset tax refunds to satisfy prior-year tax debts. The court found that the IRS’s offset procedures complied with the requirements of the Due Process Clause, as the taxpayer had received multiple notices and opportunities to contest his tax debt before the offset occurred.

The court also rejected the taxpayer’s argument that the offset violated his equal protection rights by treating him differently than other taxpayers who had not had their refunds offset. The court found that the IRS’s offset procedures applied to all taxpayers in the same way and that any differential treatment was based on differences in the taxpayers’ circumstances, such as the existence of a prior-year tax debt.

One judge, Judge Justin Walker, dissented from the majority opinion, arguing that the IRS’s offset of the taxpayer’s tax refund violated his constitutional rights to due process and equal protection. Judge Walker argued that the taxpayer’s right to due process was violated because the IRS’s notices did not provide him with enough information about the basis for his tax debt or the procedures for contesting it. Judge Walker also argued that the taxpayer’s right to equal protection was violated because the IRS’s offset procedures treated taxpayers with prior-year tax debts differently from taxpayers without such debts.

Well, there you go. I guess that’s the week.*

* ChatGPT is amazing technology and no doubt will only become more so. That said, I wouldn’t trust it to summarize D.C. Circuit opinions just yet.

Here is how Judge Walker opened his opinion in Harris v. Bowser:

Here is how Judge Rogers (joined by Judge Tatel) opened her opinion in Waterman v. IRS:

And here is the opening from Judge Walker’s dissent:

D.C. Circuit Review – Reviewed is designed to help you keep track of the nation’s “second most important court” in just five minutes a week.